Using Margin For The First Time: A Beginner’s Guide to Smart Leverage

Page Contents

Using Margin For The First Time: A Beginner’s Guide to Smart Leverage

Have you ever considered using margin for the first time to accelerate your wealth building, but hesitated because you were terrified of the risks?

You are right to respect the power of leverage. If deployed carelessly, borrowing against your securities can permanently destroy an active brokerage portfolio during a sudden market downturn.

However, when handled with strict institutional discipline, conservative margin utilization can act as an elite engine for capital velocity.

The key lies in understanding that margin is not free money for speculative gambling. Instead, it is a strategic credit facility that requires rigorous risk calculations, cost-benefit analysis, and clear cash flow exit rules.

This comprehensive guide breaks down the foundational realities of using portfolio leverage for the first time.

We will analyze how borrowing costs can make or break your strategy, how to calculate ironclad safety buffers, and how to position your debt so that you win regardless of which direction the stock market moves next.

The Absolute Basics: What is Margin?

In plain terms, margin is a line of credit provided by the brokerage provider that allows you to borrow cash against the existing value of the securities inside your investment account.

Your portfolio acts as the collateral for the loan. Because highly liquid assets back the loan, brokerages do not require extensive paperwork or credit underwriting to activate it.

When you utilize margin, your purchasing power expands instantly. This allows you to scale your asset base without being entirely restricted by your immediate bi-weekly salary deposits.

But remember, because your holdings back the loan, if the market value of your collateral falls below a specific regulatory threshold, the brokerage retains the legal right to liquidate your positions to protect the platform’s capital.

Rule #1: Audit and Compare Your Borrowing Costs Rigorously

The single biggest mistake a new investor can make when using margin for the first time is ignoring the underlying interest rate environment.

If your borrowing costs outpace the organic growth or dividend yield generated by the purchased asset, you are actively draining your wealth. Traditional retail brokerages routinely exploit uneducated investors by charging predatory, double-digit margin interest rates.

Consider the stark contrast between major financial networks. Traditional platforms like Fidelity charge exceptionally high rates for standard retail tiers.

For example, carrying a $100,000 to $249,999 debit balance at Fidelity can expose you to a base rate plus a premium that equals an effective interest charge of roughly 10.325%.

Paying over 10% in pure interest destroys your mathematical edge and represents an incredibly poor use of margin.

To maintain peak capital velocity, you must aggressively position your assets on platforms that respect your bottom line.

Transitioning your portfolio to modern tech-forward platforms shifts the numbers entirely in your favor. Modern ecosystems offer vastly superior terms for identical balance tiers:

| Brokerage Platform | Typical Margin Rate ($100K–$1M Balance) | Key Infrastructure Perks |

|---|---|---|

| Fidelity | ~10.325% Effective Rate | High double-digit retail friction blocks. |

| SoFi Invest | ~4.50% to 8.25% Scaled Rate | Highly competitive banking ecosystem integration. |

| Robinhood | 4.50% (Promos down to 4.00%) | Industry-leading rates + massive asset transfer incentives. |

Shopping around for competitive margin rates changes your math completely. Furthermore, elite brokerages frequently deploy aggressive asset-matching campaigns to capture market share.

Leveraging a 2% uncapped transfer bonus across individual and retirement accounts can net you immediate capital injections. For me, this totaled over $9,000 in raw bonuses just for migrating your existing holdings to a low-cost provider.

This is why I recommend having a Robinhood account and seeing what type of promotions they are running, as you can get a solid bonus on your account.

Rule #2: Maintain Ultra-Conservative Margin Safety Buffers

Once you secure a low borrowing cost, your absolute priority shifts to defensive risk mitigation. New traders often make the fatal error of maximizing their available leverage line, leaving their accounts completely exposed to a standard market correction. When using margin for the first time, you should strictly limit your initial draw to just **10% to 15%** of your total available purchasing power.

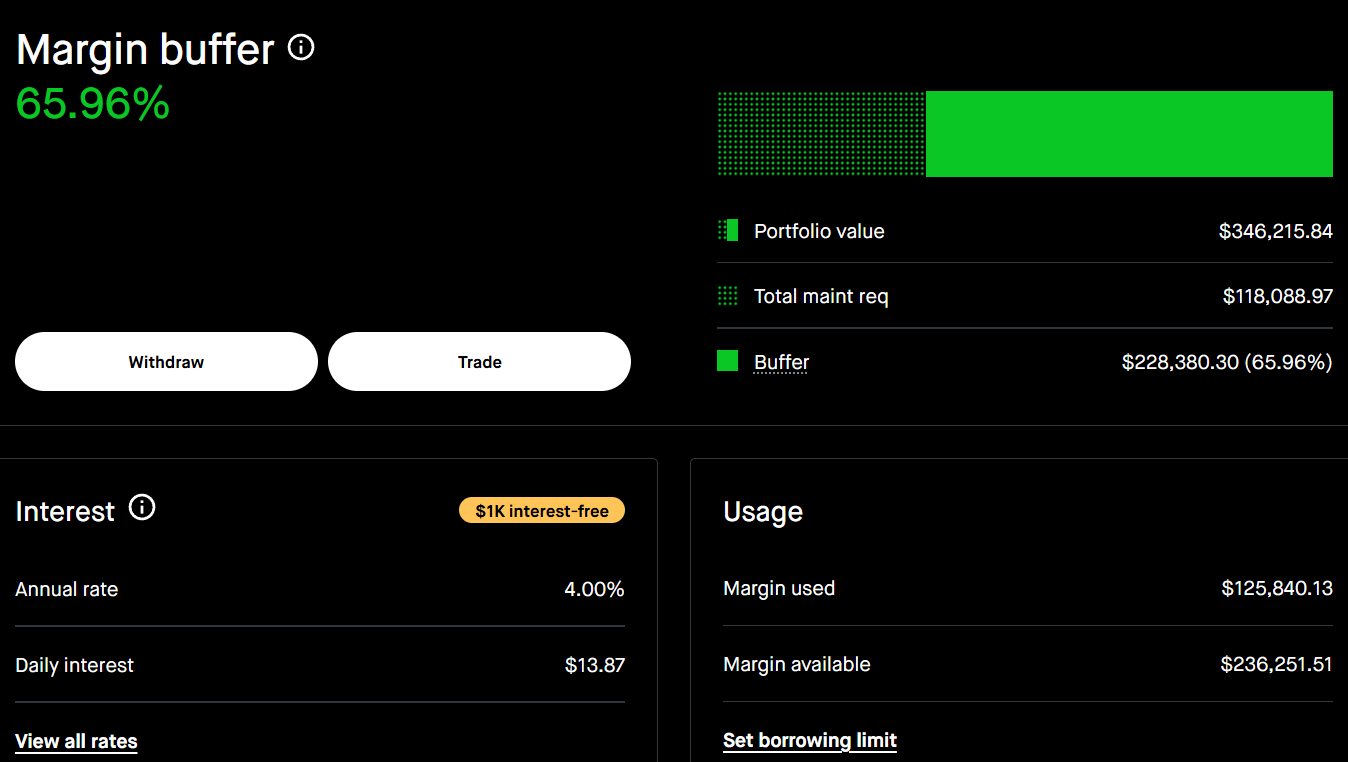

Limiting your debt footprint guarantees that your core portfolio retains an ironclad **Margin Buffer of roughly 65% or higher**. Your maintenance requirement represents the absolute financial floor your account must maintain before the system triggers an automated liquidation event. Leaving a massive premium above that floor protects your financial peace of mind.

To visualize this defense system in action, look at how a highly insulated account behaves during real-world volatility:

- Total Portfolio Asset Value: $346,215.84

- Total Maintenance Requirement: $118,088.97

- Active Margin Balance Used: $125,840.13

- Resulting Margin Buffer: 65.96% ($228,380.30 in pure safety cushion)

When you construct a 65% safety wall, a violent Friday market sell-off that drops index metrics by 4% to 5% will barely register on your risk dashboard. While over-leveraged traders panic-sell or face devastating margin calls, your conservative framework allows you to sleep soundly through temporary macro volatility.

Rule #3: Establish a Clear Real-World Exit and Reset Strategy

Never deploy margin without a definitive, rules-based payback timeline. Utilizing leverage at near market highs can be incredibly profitable, provided you possess an independent, external cash event to clear the debt slate clean. Relying on margin indefinitely turns the interest drag into an unnecessary headwind.

A phenomenal strategy for active investors is aligning a deliberate margin expansion with the pending sale of a non-liquid asset, such as an independent rental home. By deploying conservative leverage into the market ahead of time, you capture immediate asset appreciation and distribute cash flow into compounding dividend vehicles on the way up.

Once your real estate transaction closes, you take the net cash proceeds from the property sale and immediately wipe out 80% to 100% of your outstanding margin balance. This structural wipeout effectively executes a portfolio reset. If the equity markets continue to climb, you win through immediate early appreciation. If the market experiences a sharp pullback instead, your incoming real estate cash flows allow you to extinguish the debt at market lows and reset your borrowing facility to buy the dip all over again. This creates a positive outcome regardless of short-term market behavior.

Play Offense Safely to Scale Long-Term Yield

Using margin for the first time does not have to be a high-stress gamble. By systematically avoiding high-interest traps like Fidelity, anchoring your draw to a strict 10% to 15% purchasing power limit, and backing your debt with concrete real-world liquidity events, you insulate your downside while aggressively compounding your upside potential.

If you are ready to transition your assets into an optimized, low-cost environment, start exploring your options with premier digital tools. Look into maximizing your asset efficiency inside SoFi Invest to build your core portfolio foundation, or secure industry-leading margin interest brackets by deploying capital directly inside Robinhood today. Protect your capital, manage your costs, and stack your yields safely!

Click Here to Join Our Private Discord Community to access live asset breakdowns, share portfolio milestones, and master advanced covered call mechanics alongside elite yield investors today.

If this transparent look into my real income portfolio inspired you, share this article with your investment inner circle on social media right now!

Connect With Our Active Community Across Our Core Media Networks:

YouTube – Facebook – Instagram – Pinterest

![]()

Keep stacking those yields,

Brent – Investing On The Go