Covered Call ETF Income Portfolio: My $4,400+ May Dividend Paycheck

Page Contents

Covered Call ETF Income Portfolio: My $4,429.74 Passive Paycheck (May 2026)

Hey everyone, Brent here from Investing On The Go! As we officially hit the final days of May 2026, it is time to peel back the curtain. Specifically, we want to look directly at the actual cash performance of my primary income engine.

If you have been following the channel and the blog, you know my philosophy is simple. We treat our investments like a business. Consequently, this business prints predictable cash to conquer real-world living expenses.

This monthly report focuses strictly on my individual taxable brokerage strategy. Meanwhile, my tax-advantaged accounts like my traditional and Roth IRAs are much larger.

Those accounts focus aggressively on compounding long-term growth for the standard retirement age. Therefore, they are completely locked down.

As a result, you cannot seamlessly spend those retirement dividends to cover your current lifestyle today. By targeting high-yield, premium-income covered call ETFs inside a liquid taxable environment, I create an immediately accessible cash flow ecosystem. This allows me to live life on my own terms right now.

Overall, May has been an absolutely phenomenal month for capital appreciation and incoming cash distributions.

Let’s break down my automated two-account system. Furthermore, we will review my tactical mid-month asset purchases and look at the exact spreadsheet growth numbers moving into June.

📋 May Portfolio Summary

- Total Distribution Income: An incredible $4,429.74 in raw, liquid cash deposited directly into the account.

- Monthly Account Growth: The portfolio surged 5.92% over the last 30 days, representing a capital appreciation of over $20,000.

- Yearly Income Projection Jump: My forward-looking average yearly dividend baseline increased from $53,058 to $53,968, an increase of $910.

- The Automation Engine: Successfully routed distributions through a dual-account system to wipe out real-world liabilities seamlessly.

🔹 The Blueprint: My Automated Two-Account System

To pull this off efficiently, I utilize two distinct individual taxable accounts housed inside my Robinhood brokerage setup.

The first is my primary Margin Account. This is where my high-earning income streams are invested. They generate raw monthly dividend payouts and provide flexible margin access if a unique market opportunity displays itself.

If you want to create your own yield engine using the same platform I use, you can sign up for Robinhood right here to get started.

The moment these covered call funds pay out, I instantly transfer the cash into my second account. This account functions as a pure Cash Account.

While the cash sits here waiting for bills to hit, it pulls a steady 3.3% APY. This specific cash pool handles all of my automated monthly overhead. For example, my mortgage, car payment, and miscellaneous bills pull directly from this space because I cannot stack them onto a rewards credit card.

At the end of the month, the cycle completes after I fully pay down the credit cards and standard living expenses. I immediately take every dollar of remaining excess cash and send it back into the primary margin account.

Next, I use that capital to dollar-cost average (DCA) into more cash-producing shares. This action automatically expands the next month’s passive paycheck. Consequently, the layout stays entirely liquid, stress-free, and perfectly seamless.

Looking for something a bit more beginner-friendly? While I use Robinhood to run this specific margin framework, starting fresh can feel a bit overwhelming. If you want a clean, all-in-one ecosystem, SoFi is a fantastic alternative.

Their app handles your banking, credit cards, and investing inside a single dashboard. Plus, they are currently running a massive promotion.

You can secure a $25 to $425 cash bonus simply by setting up direct deposit. You can claim your SoFi cash sign-up bonus right here to launch your journey smoothly.

🔹 The Paycheck Receipts: May Dividend Distributions

Unlike traditional dividend growth strategies that force you to wait three months for a meager payout, our covered call layout relies on reliable monthly cash distributions. Here is the exact breakdown of the income checks generated by my taxable fund allocations this month:

| Payout Date | Ticker Symbol | Share Count & Dividend Per Share | Total Cash Received |

|---|---|---|---|

| May 06 | TSPY | 4,100.5731 * $0.2931 | $1,201.88 |

| May 19 | TDAQ | 4,117 * $0.3825 | $1,574.59 |

| May 20 | BTCI | 300 * $0.7934 | $238.02 |

| May 22 | IWMI | 2,092 * $0.6046 | $1,264.82 |

| May 22 | IAUI | 271 * $0.5551 | $150.43 |

| Total Passive Monthly Income: | $4,429.74 | ||

Pulling in $4,429.74 in a single calendar month completely illustrates the raw capability of a mature income ecosystem. When you intentionally engineer your portfolio to deliver high-yield cash flow every few weeks, your reliance on selling principal shares drops to zero.

Ultimately, that is how you build a permanent margin of safety.

🔹 DCA Logic: May Trade Log & Analysis

My logic for weekly buys is dead simple. I consistently scale my positions by buying where I see the absolute best relative value at that specific moment. Furthermore, I do not care if the broader market is hitting all-time highs.

Today’s highs are simply tomorrow’s potential lows or prices we may never see cheap again. Therefore, you cannot time the macro environment, but you can always control your consistency.

As documented in my tracking spreadsheet above, my primary focus throughout May was aggressively targeting TDAQ. Specifically, my goal was to scale this position up to mirror my 4,100-share TSPY core block.

You can see this executed cleanly on May 11th with a dominant 132-share purchase at $28.81. This move placed $3,733.38 of capital to work right before major ex-dividend dates locked in.

In addition, you will notice dollar cost averaging on May 28th, which was a buy into IAUI at $54.44. Gold took a sharp asset correction recently. Consequently, it created a beautiful 4% to 5% dip from my initial exploratory position.

I immediately stepped into dollar-cost averaging. This move brought my overall cost basis down smoothly while expanding my alternative asset income layer.

With those final purchases settled, I am officially done buying for the month.

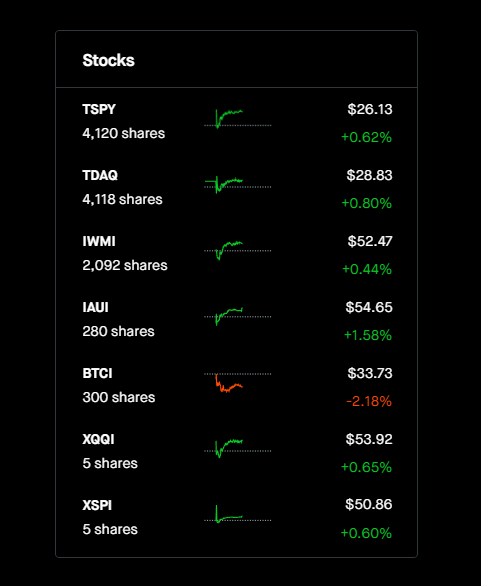

🔹 Current Taxable Account Balance and Holdings View

To give you a comprehensive look at how these assets sit altogether inside the dashboard, here is the official status of our taxable stock portfolio as of May 31st, 2026. This layout matches the dashboard view displayed on my Robinhood portfolio.

Our current holdings stack up aggressively. As seen above, our foundational footprint centers around heavy allocations in major yield engines.

First, we have 4,120 shares of TSPY sitting at a market price of $26.14. This matches perfectly with 4,118 shares of TDAQ valued at $28.82.

Backing those positions up is our massive block of 2,092 shares of IWMI at $52.50. Additionally, we hold 280 shares of IAUI and our combined 300 shares of BTCI, navigating the gold and crypto-yield layer.

This concentrated income mix has allowed the entire portfolio to capture massive upward market momentum. For example, over the last month alone, the account surged an astounding 5.95%. This translates to over $20,000 in clean capital appreciation.

📊 Tracking the Mathematical Progress

To close out the month, I want to show you the power of tracking your data over time.

When I opened my tracking spreadsheet at the beginning of May, my portfolio metrics showed an average monthly income of $4,421.55. This was tracking toward a forward-looking yearly baseline of $53,058.54.

Because of our systematic monthly cash re-injections and targeted asset accumulation, look at where those numbers stand today at the end of May:

• Average Monthly Baseline: Climbed to $4,497.40

• Projected Yearly Income: Surged to $53,968.78

That is an absolute increase of $910.24 in predictable yearly income added to my life in just 30 days of mechanical execution.

This is the exact blueprint of how you scale an income empire. We do not gamble on hype, and we do not time volatile swings.

Instead, we systematically construct a bulletproof income waterfall that compounds larger and larger every single month.

If you want to discover more advanced strategies for securing your financial foundation, check out our comprehensive breakdown on life insurance and wealth building.

Building a permanent asset foundation requires covering all entry points. Additionally, securing a liquid backup fund is crucial for safety.

You can read our guide on how to build a 3-6 month emergency fund right here.

🚀 Scale Your Monthly Brokerage Paycheck

Are you exhausted from watching your wealth sit idle in low-yield traditional spaces? Or are you tired of trying to perfectly time complex swing trades? The goal of our movement is absolute clarity. We want to build a reliable cash-flow matrix that gives you the ultimate freedom to handle your bills, leave the daily grind behind, and live life entirely on your own terms.

👉 Click Here to Join Our Private Discord Community to access live asset breakdowns, share portfolio milestones, and master advanced covered call mechanics alongside elite yield investors today.

If this transparent look into my real income portfolio inspired you, share this article with your investment inner circle on social media right now!